How do you determine when to sell your apartment building to maximize the overall returns? I’m going through this decision-making process right now for one of my buildings, and I’d like to share with you my thinking.

As always, there are multiple factors that go into deciding if it’s right to sell the building now or later:

- Have you created most or all of the value there is to create?

- How attractive is the future cash-on-cash return?

- What do you expect the market to do? Are values likely to increase or decrease?

- What yields a higher return? Selling, holding, or refinancing?

Let’s apply all 4 criteria to my situation.

I purchased a 12-unit building with rents far under market. Three years later, income is about 35% higher than before. In my estimation, we created about 95% of the value there is to create.

Future cash-on-cash return is not that great at all; it’s estimated only at about 7% per year. This was planned from the start: I knew the value would be created by raising the rents, not so much from cash flow. Regardless, cash flow moving forward will not be stellar.

The market is stable. It’s tough to tell what cap rates will do. On the one hand, as interest rates will inevitably go up, so will cap rates, and valuations will drop. On the other hand, multifamily assets are so hot that the demand may counteract any rise in interest rates. Overall, I think the market is stable. In other words, I’m not seeing any massive upside coming from the market.

What Yields a Higher Return: Selling Now, Selling in 3 Years, or Refinancing?

In order to answer this question we need to consider the Internal Rate of Return (IRR).

I normally don’t talk about the IRR because it’s one of those complicated concepts that tends to confuse investors, and it’s rarely used for simple scenarios like buying and selling something.

But when it gets more complicated, like refinancing something, where capital is invested then partly returned and then ultimately sold, using an average annual return stops working. The reason for that is that your invested capital changes in a refinance scenario.

Let’s say you and your investors put in $100,000 to purchase a building. After you’ve created a bunch of value in 3 years, you decide to refinance and return $75,000 of the invested capital back to the investors. Due to the higher debt service, your cash flow is reduced, but because you only have $25,000 of capital in the deal, your cash-on-cash return sky rockets. In fact, at that point, the cash-on-cash return and average annual return become meaningless.

That’s where the IRR comes in. The IRR takes into account:

- Capital going into and coming out of the investment, one or more times;

- Cash flows generated by the investment; and

- The passing of time.

The passing of time is important because money loses its value over time. For example, you getting $10,000 TODAY may mean a lot more to you than the promise of $50,000 in 5 years, right?

The IRR takes the passing of time into consideration (through some magic I don’t quite understand, but it makes sense). The IRR is the great equalizer that allows you to compare totally different investments in an apples-to-apples way. You could calculate the IRR of investing in gold vs. commercial real estate, and the IRR would give you an intelligent metric for calculating the better investment. It’s crazy.

Your objective with this exercise is to calculate the IRR for each of the different scenarios we described above (sell now, sell later, or refinance and sell later). Once we have the IRR for each scenario, we can more easily compare them to each other.

The first thing you’ll need is a detailed financial model that calculates all of the cash flows from your investment, as well as any proceeds coming from the refinance and the ultimate sale.

This is obviously easier said than done, but I’m going to assume you have built or purchased a financial model to let you model this… if not, build or purchase one (like the “Syndicated Deal Analyzer“).

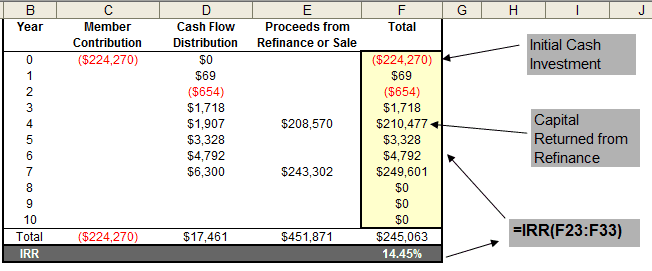

To demonstrate how to calculate the IRR using Excel and your financial model, you create a table like the one below:

It’s a simple table (though the numbers in it can be complex to determine — that’s why you need a good financial model!) that shows the initial cash investment, the cash flow distributions, and any return of capital (from refinance or sale). In the scenario above, we’re doing a cash-out refinance after Year 3 and then selling after Year 7.

Once the cash flowing into and out of the investment is defined (in Column F), you can then apply the Excel function “IRR()” to that column, and it magically calculates it for you.

Using my deal analyzer, I have modeled these 3 scenarios and determined the IRR for each. Here are the results:

- If we sell after Year 3 (after we’ve built most of the value by increasing rents to market), the IRR is 13.25%.

- If we hold a couple of more years and sell after Year 5, the IRR becomes 9.54%. Why does it drop? Because the little bit of extra cash flow and the passing of time actually decreases our returns.

- What if we refinance After Year 3, return most of the invested capital and ultimately sell after Year 7? This is normally my favorite strategy to boost returns but in this case the IRR is only a paltry 8.94%, the lowest of the three. The reason for that is the low cash flow with this building. After refinancing, the cash flow is even further reduced, putting extreme pressure on the IRR as time passes without any additional upside.

Based on this, the IRR analysis is telling us to sell after we’ve built all of the value, confirming our suspicions from earlier.

If the cash flow were better in this building (like at least a 10% cash on cash return), this scenario could look quite a bit different. Most likely, refinancing (Scenario # 3) would produce the highest returns. This would make your investors happy because they get all or most of their investment back and you get to hold on to the building for as long as you want.

Conclusion

Deciding to sell a building is never easy, especially if you’ve grown accustomed to the income. It also depends on what kind of lifestyle you want: if you want to maximize returns, you’re constantly crunching the numbers and buying and selling accordingly. On the other hand, you may prefer the more passive route and be less transactional (and busy!), but perhaps not squeeze the highest returns out of your investments.

What are YOUR criteria for deciding when to sell a piece of property?

One Response